Checking in on Wisconsin banks

It’s hard to fault anyone who saw news of Silicon Valley Bank’s failure in March and had flashbacks to the onset of the Great Recession.

It wasn’t hard to imagine the bank’s failures leading to troubles for hundreds if not thousands of businesses and their employees. Add in the failures of Signature Bank and First Republic, plus recent news that PacWest is considering a sale, many are worried about a contagion in the banking sector, which would have a devastating impact on the economy.

Nearly half of Americans say they are concerned about the safety of their money at banks or other financial institutions, according to a recent Gallup poll.

The growing concerns about the banking sector have some remembering what happened in 2008. It took time to unfold. Bear Stearns failed in March of that year, but the bankruptcy of Lehman Brothers and bailout of AIG didn’t take place until September.

Despite growing concerns for the U.S. banking industry, in Wisconsin, many bankers express confidence in the strength of the banking sector and point to their steady, more conservative approach to business and focus on customer relationships as reasons they are well positioned.

“People need to realize that all banks are better capitalized with stronger balance sheets than they were heading into the Great Recession. This is especially true of Wisconsin banks/banking,” said Mike Daniels, president and chief executive officer of Green Bay-based Nicolet National Bank.

Others also described Wisconsin’s banks as strong and on solid footing or noted the state has well-run companies, strong business leaders and a growing economy.

“The people of Wisconsin can take comfort in knowing our sensible, Midwest approach to business carries through to the way our banks operate,” said Bryan Johnsen, executive vice president and chief financial officer at Oak Creek-based Tri City National Bank.

“Overall, I view our state as a bit more conservative, which tends to avoid the highs and lows of some other markets,” said Kevin Kane, southeastern Wisconsin market president at Madison-based First Business Bank.

Wisconsin banks also generally look much different than Silicon Valley Bank, which had grown to more than $200 billion in average assets by the end of 2022. While U.S. Bank and BMO Harris Bank – both of which have a significant presence in Wisconsin – are larger, the biggest Wisconsin-based bank is Associated Bank, with just under $40 billion. Interestingly, a decade ago, Associated and SVB were nearly identical in size based on average assets at around $23 billion.

Fueled by deposits from venture capital-backed firms that were in turn invested in securities with longer-term maturities, SVB’s rapid growth posed a challenge for regulators, a Federal Reserve review of the failure found. The review also highlighted that SVB’s board and management failed to manage their risks.

“Managing a bank is never easy,” said David Schuelke, CEO of Brookfield-based Spring Bank. “The failure of SVB highlighted a few of the issues that banks face each day. Those being managing liquidity and the bank’s investment portfolio.”

Among the issues identified in the Federal Reserve review were incentives focused on short-term profits, using less conservative stress testing assumptions to mask risks, making counterintuitive modeling assumptions about the duration of deposits and removing interest rate hedges.

“In sum, when rising interest rates threatened profits and reduced the value of its securities, SVBFG management took steps to maintain short-term profits rather than effectively manage the underlying balance sheet risks,” the Federal Reserve review says.

To get a clearer picture of the health of southeastern Wisconsin’s banking sector, BizTimes Milwaukee reached out to more than 30 banks in the region with a series of questions about what doing business has been like since SVB’s failure, the impact of rising interest rates, potential for additional regulation and other areas of concern, like stress in commercial real estate. In total, 14 responded.

Many reported taking additional customer calls in the aftermath of SVB. Others took the opportunity to reach out. They all highlighted the importance of having a relationship with their customers.

“It’s been an interesting several weeks, to be sure,” said Jim Popp, president and CEO of Racine-based Johnson Financial Group. “Technical things that we as bankers think about all the time – like capital ratios and liquidity – have become part of the discussion in coffee shops, sporting events and everywhere else. These are complex issues, and we’ve tried hard to provide all the transparency necessary to tell the story and present the strength and stability of our position without getting too deep in the weeds.”

The following are excerpts from responses provided by leaders of banks with a presence in southeastern Wisconsin:

BizTimes: Have you changed anything in the way you operate following the failure of Silicon Valley Bank?

Jim Popp, president and CEO, Johnson Financial Group: “We have not changed any of our fundamental, everyday processes or procedures. If we were watching inflows and outflows of deposits daily, we probably watched them hourly for the first several days after the news broke. Other than that, the news really hasn’t changed the way we are doing things.”

Scott Huedepohl, president and CEO, Community State Bank: “Not really, we only invest in very safe instruments that provide cash flow for us on a regular basis. Every bank, insurance company and mutual fund has invested in lower yielding investments that they wish they didn’t have, but those investments only lose money if you sell them.”

Jay McKenna, president and CEO, North Shore Bank: “North Shore Bank follows the same safety and soundness practices and high-touch customer service principles that have built thousands of trusted personal and business relationships throughout our history.”

Mike Daniels, president and CEO, Nicolet National Bank: “No – it is business as usual for us.”

Scott Cattanach, president and CEO, Peoples State Bank: “Peoples regularly balances risk contingencies with customer needs, so nothing significant has changed specifically following the SVB failure. However, since interest rates began to increase in early 2022, we have reduced our purchase of new securities and targeted new securities with faster repayment speeds to reduce our exposure to unrealized market value losses.”

Edward Schaefer, president and CEO, First Federal Bank: “Not really.”

Kevin Anderson, market president and business banking president, Old National Bank: “No. The collapse of these niche institutions affected the operating environment for all banks. Specifically, it shined a spotlight on some traditional areas of strength for ONB, including granular deposits and loans (meaning we have many smaller-sized deposit accounts and a diverse balance sheet with an average loan size of approximately $1 million), low loan-to-deposits ratio, strong credit underwriting and low loan charge-offs.”

Steve Schowalter, executive chairman and CEO, Port Washington State Bank: “Certainly larger transactions get more review and scrutiny to determine if it is something in the ordinary course of business for an institution of our size or if it is something that warrants a contact to the customer or company to determine if there are any questions or concerns. Money is certainly moving around due to the rate environment and all banks are more protective of their core deposit base as those monies are generally less expensive than brokered or borrowed funds.”

BizTimes: What are the specific actions you and your bank take on a day-to-day basis to manage cash inflow and outflow?

Jay McKenna, North Shore Bank: “Our finance team tracks our liquidity positions in real-time. That along with planning for the inflows and outflows of the business allows us to be prepared for both the short- and long-term cash flow situations.”

Scott Huedepohl, Community State Bank: “We manage cash flow every day and have forever. We have taken a conservative approach in what we invest in. Whenever you have rapid rate adjustments you have to just spend more time on it.”

Mike Daniels, Nicolet National Bank: “We certainly prepared for the potential of some deposit outflows, which we never materially saw. It makes sense for all banks to have a deep understanding of their liquidity sources in a crisis, so what happened gave us a chance to go back and review those. While we were prepared, nothing really materialized.”

Scott Cattanach, Peoples State Bank: “Our bank has long maintained liquidity contingency plans to support our normal and stressed operations, and we have always conducted quarterly liquidity stress tests. As part of our normal daily procedures, our CFO reviews our listing and maturity of out-of-area funding sources and works with our lending team to project cash and liquidity needs.”

John Hazod, regional chief financial officer, Town Bank: “The key component for managing cash inflow and outflow is having an understanding of your customer base and remaining in constant communication with our clients. We keep abreast of market trends relative to interest rates to ensure we offer competitive interest rates on deposits and loans. Our management team operates the bank in a conservative manner to ensure the bank maintains appropriate levels of liquidity to meet our clients’ cash needs.”

Greg Larson, CEO, Ixonia Bank: “We take very seriously the responsibility to meet the financial needs of our customers and the expectation that we will be there whenever called upon. That drives us to ensure we are well capitalized and ready with the resources, services and products necessary to take care of the financial needs of the people and businesses we serve.”

Jim Popp, Johnson Financial Group: “At JFG, we have always kept an eye on day-to-day cash inflows and outflows as a part of our daily process. In fact, it’s not uncommon for us to see swings in liquidity from time to time for various reasons, some related to customer activity and some related to our own balance sheet management. We model various interest rate, capital and liquidity scenarios regularly and operate with a robust set of protocols in place to help us manage our positions actively. We obviously can’t think of everything, but our team works very hard to create as predictable a set of outcomes as possible.”

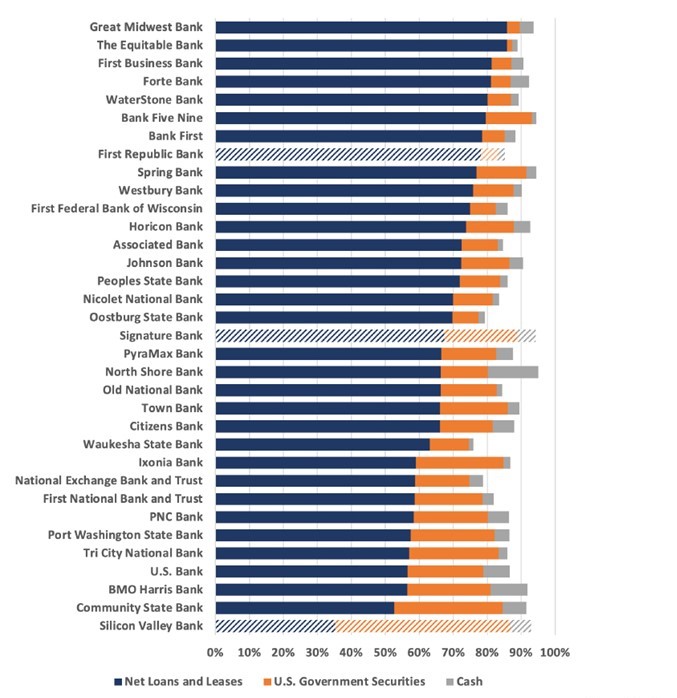

Bank Balance Sheet Mix

One of the issues contributing to Silicon Valley Bank’s failure was the amount it invested in government securities. While a generally safe investment, rising interest rates meant that securities purchased with lower rates lost their value if the bank wanted to sell them. Graph data is as of Dec. 31, 2022, with recently failed banks highlighted.

BizTimes: How has the ease of transacting with technology changed the way your bank operates?

Scott Huedepohl, Community State Bank: “You have to offer the products and services that our customers want which includes technology that makes it easy to transact business. Where in the past when someone wanted to take money out you knew about it, while today you might not until it has happened.”

David Schuelke, CEO, Spring Bank: “We recognize that clients can move balances more quickly, but aside from reducing the transactions completed through a personal banker, we haven’t changed in significant ways in how we operate.”

Scott Cattanach, Peoples State Bank: “The ability to move money digitally can increase the potential liquidity volatility associated with large deposits held by retail customers, but digital tools can also make business deposits more stable as our technology tools are closely tied to their invoice collection, accounting and fraud systems.”

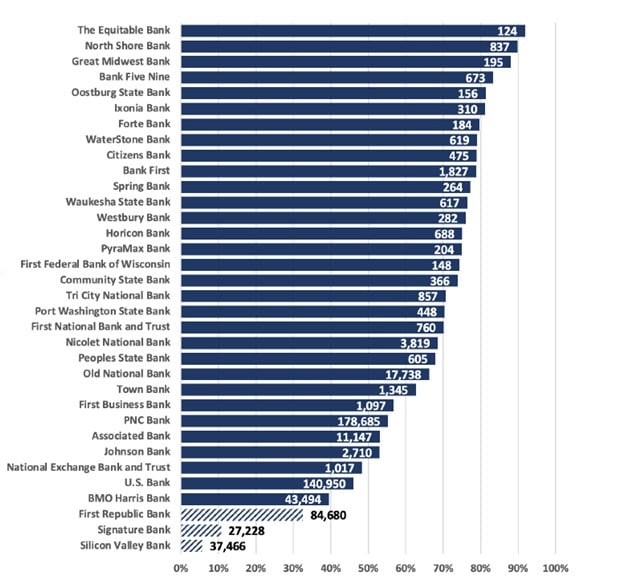

Estimated percentage of insured deposits and number of deposit accounts exceeding $250,000

Insured deposits: Silicon Valley Bank’s failure put a spotlight on the FDIC’s deposit insurance, as around 5% of its deposits were insured and nearly 37,500 of its accounts exceeded the $250,000 threshold. The percentage of insured deposits and number of accounts exceeding the threshold can be shaped by a variety of factors, including customer mix. There are also many ways to increase the insured total beyond $250,000.

BizTimes: How have rising interest rates altered your strategy in allocating your balance sheet?

Bryan Johnsen, executive vice president and CFO, Tri City National Bank: “There is uncertainty on what the Federal Reserve may do and how the economy reacts to the rapid increase in rates. We are taking a cautious approach with liquidity planning.”

Jay McKenna, North Shore Bank: “Going back a year or two, we saw rates rising significantly and made a decision to ‘keep our powder dry’ for investment purposes and stayed more in cash. This may have hurt our earnings a bit at the time, but it has paid off in the longer term.”

Kevin Kane, southeast Wisconsin market president, First Business Bank: “Unlike most banks, we don’t attempt to capitalize on the typically upwardly sloping yield curve by lending longer and funding shorter term. We don’t believe in taking interest rate risk as we can’t control or even affect interest rates, and we don’t like banking on (no pun intended) things we can’t control or at least affect. Additionally, we have always tried to maintain a smaller shorter-duration investment portfolio as we earn more for our shareholders by allocating our assets to making commercial loans, which we believe is our core competency, so that hasn’t changed either.”

David Schuelke, Spring Bank: “In a rising interest rate environment, net interest margins are squeezed, but our strategic focus doesn’t change. Within our loan portfolio we have been leaning towards more floating-rate loans versus fixed-rate loans in the current environment.”

Scott Cattanach, Peoples State Bank: “While the business press has talked a lot about these balance sheet impacts, the banking industry is simply doing what it was designed to do: be a financial intermediary. … To help offset the negative impacts of acting as the rate change intermediary for customers, we have invested in securities and business loans with shorter fixed-rate periods, typically fixed for the first five years or less.”

Steve Schowalter, Port Washington State Bank: “Rising interest rates have certainly impacted balance sheet strategies. At this point in time, as our lower yielding bond portfolio amortizes and matures, the funds are being redirected into lending of all types at better rates to offset the increase in deposit costs. As a community bank, we originate all categories of loans with an emphasis on residential mortgage lending. When long-term fixed rates started to rise, we found renewed interest in variable-rate loans, which we are funding both with cash on hand and maturing bond portfolio dollars.”

Tom Richtman, Wisconsin commercial banking head, U.S. Bank: “We are focused on the strength and stability of our balance sheet, ensuring that we continue to have healthy liquidity levels and to do the right thing for the communities and constituents we serve. Key to that is the strength of our well-diversified deposit base and business mix across consumer, corporate and commercial clients and services. If the industry disruption in March showed us anything, it’s that our long-term planning efforts contributed to our resiliency during times of uncertainty.”

BizTimes: Do you expect to see regulatory changes in the wake of the SVB failure and as a result of the industry turmoil? If so, what changes do you expect or want to see?

Jim Popp, Johnson Financial Group: “It’s hard to speculate about what changes we might see but safe to assume that the regulatory environment is not likely to soften in the near future.”

Kevin Kane, First Business Bank: “Yes, it’s a bit of a natural reaction, and there will certainly be more rigorous regulations, like stress testing for large regional banks. More so, we would expect regulators to be more diligent on digging into the interest rate risk and related mitigation strategies at all banks, not necessarily through new regulation, but as part of the normal exam process.”

Bryan Johnsen, Tri City National Bank: “I expect a refresh on how the regulators view deposit modeling assumptions in different rate environments.”

Jay McKenna, North Shore Bank: “Bank regulators in recent years have been appropriately focused on interest rate and liquidity risk. I expect that to continue. The banking industry continues to be in excellent shape, so I don’t expect any drastic changes to the community bank sector from a legal or policy standpoint.”

Mike Daniels, Nicolet National Bank: “I think increased regulation will be two-fold. First, larger banks will be more heavily regulated, and rightfully so. Whether that is banks above $100 billion, $50 billion or something else, I think all of those banks are preparing for additional scrutiny from regulators. Second, the SVB failure shone a spotlight on bank liquidity. Again, this really isn’t a concern for community banks, but we see the regulators either imposing additional liquidity requirements or guardrails in place, or placing much greater emphasis on that area when banks undergo their regulatory examinations.”

David Schuelke, Spring Bank: “My position is that the banking industry is highly regulated today. SVB had a unique business model. Additional new regulations would be costly. Bank clients will bear a portion of the cost, which hurts consumers. The failure of SVB will cost the FDIC insurance fund billions of dollars. The FDIC insurance fund is supported 100% by banks, not taxpayers. A special assessment will most likely be required to replenish the insurance fund. I want to see a special assessment placed on large regional and large national banks. Community banks should be spared the cost of a special assessment.”

Scott Cattanach, Peoples State Bank: “There appears to be momentum to move today’s ‘biggest bank’ special regulations to the smaller asset-sized regional banks. That said, I don’t believe community banks with assets under $10 billion will see much change based solely on what has happened recently. However, I would not be surprised if the FDIC insurance limit was increased, even to reflect inflationary impacts, since it last was increased in 2010. A case can be made for the benefits of a $500,000 FDIC insurance level.”

Steve Schowalter, Port Washington State Bank: “I don’t expect many regulatory changes in the wake of SVB but perhaps increased emphasis by examiners on the stress testing and best practice guidance already out there, at least that would be my hope.”

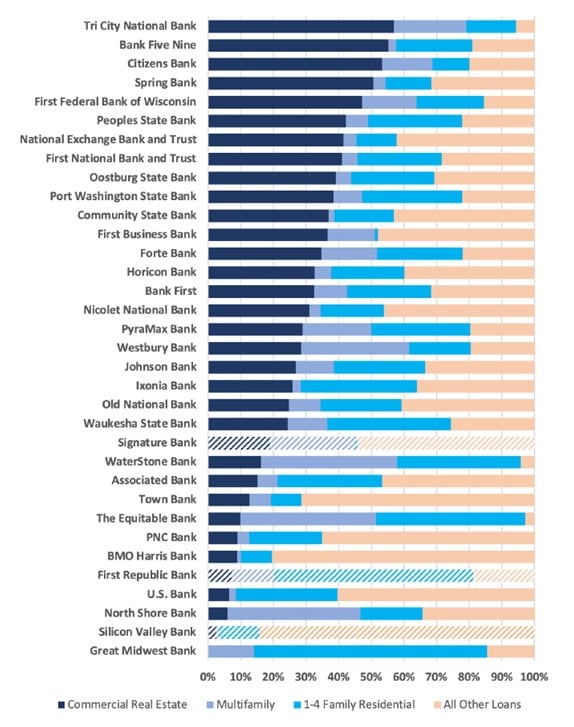

Bank loan mix

Commercial real estate, especially office buildings, is one potential area of concern for the banking sector moving forward. This graph, with data from Dec. 31, 2022, shows how area banks have allocated real estate loans as a percentage of their total net loans and leases.

BizTimes: Do you anticipate customers moving toward large banks in the wake of the SVB failure? What kind of challenge does that pose for regional and community banks?

Kevin Anderson, Old National Bank: “Just the opposite, we see clients moving to banks like ours who have a solid history.”

Tom Richtman, U.S. Bank: “While movement may have happened at a larger scale across the banking industry in the wake of the events in March, we’ve seen more and more clients – whether individuals, families or businesses – looking to earn more on their deposits due to rising interest rates as well as identifying banks that offer them the stability they are looking for.”

Bryan Johnsen, Tri City National Bank: “There will always be trends in customer behaviors. I’m confident that community banks have a lot to offer and will prosper as a vital role in any community for a long time.”

Scott Huedepohl, Community State Bank: “Community banks have been the cornerstone of most small- to mid-sized towns in America. We tell our customers what we will do and, more importantly, will not do with their money when they trust us with it. … I see it going the other way in fact and you will see community banks continue to grow.”

Mike Daniels, Nicolet National Bank: “Yes, there was some deposit outflows from community banks last quarter, but not nearly to the degree that people were concerned with. … I really think you’ll see some of that money come back to community and regional banks given the rates they are paying over the large banks. It is important to understand that community banks are safe and offer a value proposition that many of the large banks cannot.”

John Hazod, Town Bank: “There may be some movement of funds to larger banks; however, we anticipate that to not significantly impact our financial institution. … Wintrust has a granular consumer and business deposit portfolio and does not have any material, at-risk deposit concentrations. … Regional and community banks play a critical role to small businesses and consumers. Local banks have built strong relationships with their client base as these banks have and will continue to be an important component to the economic strength and growth of the communities they serve.”

Jim Popp, Johnson Financial Group: “We have seen and heard of customers moving to the perceived safety of large banks in the wake of SVB. At JFG, we haven’t experienced any major outflows related to the SVB news. For the regional and community banks who have strong liquidity and capital positions, the challenge is to explain a complex issue to customers who, by all rights, shouldn’t need to worry about those things.”

BizTimes: The past few years have brought many changes to the commercial real estate world. Do you see increased risk for banks with office buildings being distressed?

Tom Richtman, U.S. Bank: “Commercial real estate is an area of a lot of emphasis and focus for the banking industry as a whole as there’s activity occurring in tenant and sponsor behavior changes. It’s something that we are focused on as well. However, as a company, we have been prudent in our approach in the commercial real estate space. Commercial real estate makes up 2% of our total loans.”

John Hazod, Town Bank: “The commercial real estate segment has been challenged over the past few years due to COVID. Most banks maintain a diversified loan portfolio that should mitigate the potential exposure to certain asset classes. A key component is identifying the risk profile of the portfolio, engaging with your clients and remaining in communication on the status of repayment ability and understanding the strategies to maintain an appropriate level of debt relative to the collateral value.”

Kevin Kane, First Business Bank: “If banks haven’t been careful about who they partner with, haven’t spent the time to get to know an owner or developer, or go into markets they don’t understand, perhaps that creates risk for them in certain asset classes like office buildings. We see this as an issue in the very large urban markets on very large office towers. A lot of this debt is held outside of the banking system and given the size of those loans, what is held at banks is primarily at the large institutions.”

Mike Daniels, Nicolet National Bank: “Yes, but much more so for banks that have office exposure in larger cities. As our markets are almost exclusively small- and mid-sized cities and towns, our office exposure is minimal. While it is something we are watching, we are not overly concerned at this point.”

Edward Schaefer, First Federal Bank of Wisconsin: “The office market appears to be tough. Also, a lot of low-rate commercial real estate loans are going to reprice in the next two years. We have a diversified commercial and residential real estate loan portfolio that is quite strong.”

Jay McKenna, North Shore Bank: “We have very little exposure to this sector, but it certainly seems that there may be some stress there around the country. Generally speaking, banks are very well capitalized today so hopefully the situation can be managed without too much disruption to the broader economy.”

Scott Huedepohl, Community State Bank: “It’s obvious just driving around that many of these buildings are not filled. Diversification is key to working through any collateral types over time. The majority of our commercial real estate is owner-occupied which helps a lot. This was done on purpose as it reduces the risk. Ten years from now it will be something else causing heartburn, so don’t put all your money into one industry.”

BizTimes: Given uncertainty in the general economy and issues raised by the SVB failure, are you tightening or making any changes in your approach to lending and credit?

Kevin Kane, First Business Bank: “We want to be consistent. To be a good banker means to understand and get to know the people, businesses and sectors you work in and stick with fundamentals in terms of underwriting and risk management.”

Bryan Johnsen, Tri City National Bank: “We maintain the same credit standards regardless of the economic outlook. It’s a big reason we have continued to grow throughout our 60 years. There has been less deal flow because of the higher rate environment, so I expect loan growth to slow in 2023 compared to 2022.”

David Schuelke, Spring Bank: “We have not tightened significantly in our underwriting of new commercial loan opportunities. Spring Bank is giving greater attention to maintaining our net interest margins and adjusting loan pricing for risk given existing economic forecasts.”

Scott Cattanach, Peoples State Bank: “Our changes were in ways that increased customer options and enhanced our risk position. For example, we launched a new SBA 7a guaranteed loan program to provide an additional source of credit during volatile times or declining collateral values so locally owned businesses can continue to grow.”

Edward Schaefer, First Federal Bank of Wisconsin: “Not really, but with interest rates increasing we must stay focused on our net interest margin. Customers have not seen loan rates in the 6%-9% (range) in years.”

Steve Schowalter, Port Washington State Bank: “As for any changes in our lending and credit decisions given the economy and rate environment, they are few. We have increased owner equity requirements in some categories of lending and are likely more proactive with borrowers exhibiting stress or unusual late payment habits.”

Jim Popp, Johnson Financial Group: “As lenders, we talk a lot about the need to be consistent in our approach. We can’t turn it on when things are good and turn it off when things get tough. If we stay consistent in how we approach risk, underwriting and our overall credit process, we don’t need to change much in reaction to changes in the economy.”

Sizing up southeast Wisconsin banks: Banks serving southeastern Wisconsin come in a wide range of sizes with many of them much smaller than Silicon Valley Bank and other banks that have failed recently. Others not on this list include JPMorgan Chase and Wells Fargo. Data on deposit growth includes acquisitions. Banks in bold provided responses to BizTimes Media’s questions on the health of the sector.

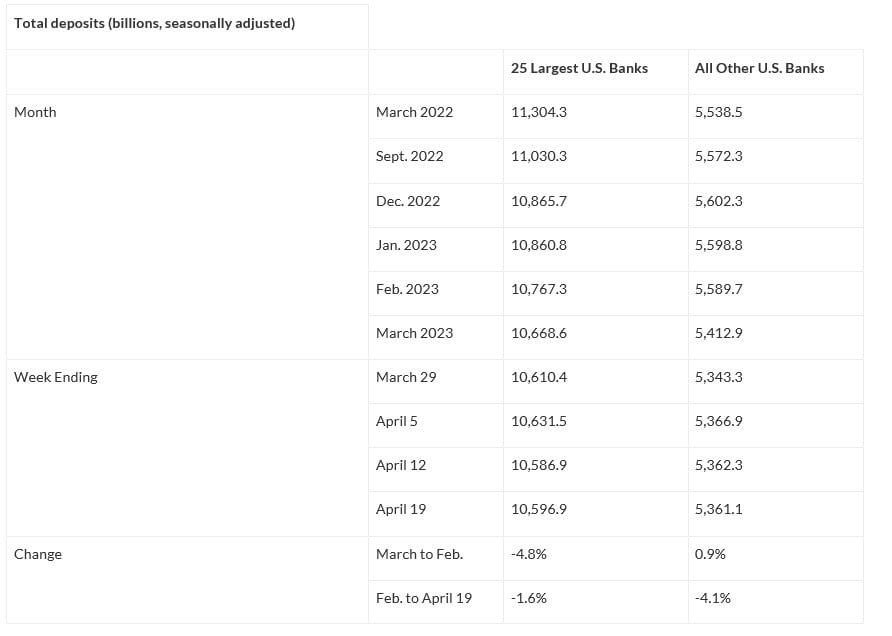

Shifting Bank Deposits: The failure of regional banks like Silicon Valley Bank has fueled speculation that consumers will shift deposits to larger banks. While many Wisconsin bank leaders think their higher rates and customer relationships will win out, there is some evidence of a shift to larger banks in Federal Reserve data. Deposits have been trending down as consumers deal with inflation. From March 2022 to February 2023, the decline was faster at the 25 largest U.S. banks, but since February, the rate of decline has been faster at all other banks.