SUMMARY

If you’ve been asking yourself "what is house hacking" after hearing about it on the news or while scrolling your social media feeds, you're not alone. This buzzworthy strategy is transforming how people approach homeownership and wealth-building, especially for first-time homebuyers. Learn more about how this unconventional approach is helping thousands slash their housing costs and build equity faster.

Picture this: You're hanging out with your friends and someone casually mentions they're living rent-free in their own house. Your first thought? "Yeah right.” But then they explain they bought a duplex, live in one side, rent out the other and their tenant's rent check covers their entire mortgage. Suddenly, they're building equity instead of burning money on rent and you're sitting there wondering why nobody told you about this earlier.

That's house hacking.

What is House Hacking?

At its core, house hacking is the strategy of buying a home, living in part of it and renting out the other parts to cover your mortgage and expenses. Think of it as leveling up from "splitting rent with roommates" to "having your tenants pay your mortgage while you build equity."

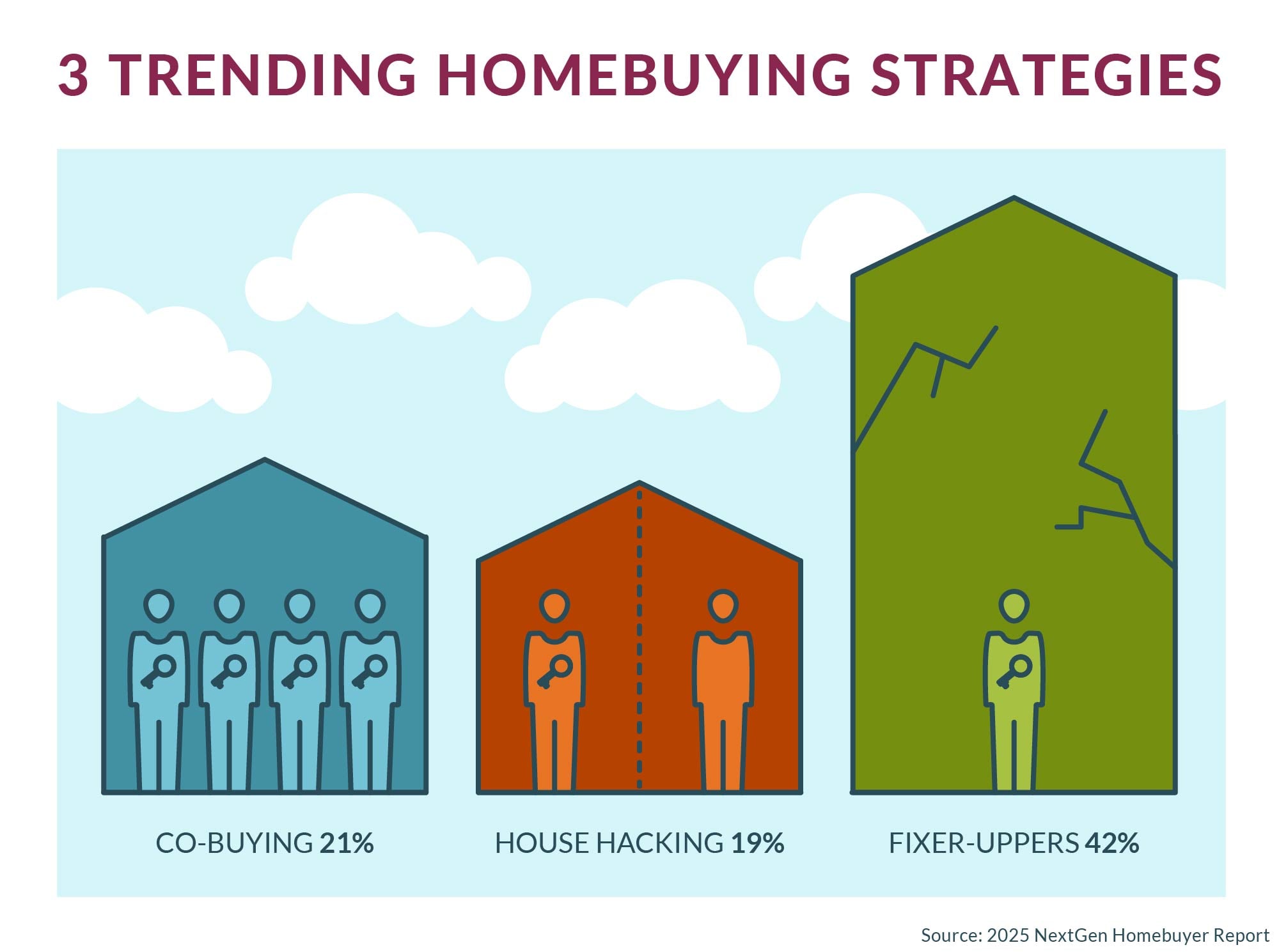

Comparing House Hacking, Renting and Buying

Okay, so you're probably wondering how house hacking stacks up against your current situation (hello, overpriced apartment) or traditional homebuying. Let's break it down:

| Method |

House Hacking |

Renting |

Buying |

| Monthly Cost |

Low to $0 |

High (Standard Rent) |

Moderate (Traditional Mortgage) |

| Equity/Wealth Building |

High (Rapid) |

None |

Moderate |

| Maintenance |

High (Landlord Duties) |

None |

Moderate |

| Privacy |

Low to Moderate |

High |

High |

| Financing Type |

Owner-Occupied |

None |

Owner-Occupied |

The Most Popular House Hacking Strategies

There are a few different paths you can take, each with its own vibe and requirements. The key is figuring out which one fits your lifestyle and your local market.

Pro Tip: Discuss with your loan officer and REALTOR® about any local restrictions or regulations before you commit to a strategy.

1. Multi-units

This is the "gold standard" of house hacking. You buy a duplex, triplex or fourplex, claim one unit as your own and rent out the others. No awkward kitchen encounters at midnight. No fighting over bathroom time. Just you in your unit, collecting rent checks from the people next door.

2. Accessory Dwelling Units (ADUs) and “Flex Spaces”

Can't find a multi-unit in your favorite neighborhood? No problem. Look for single-family homes with "ADU potential" — basically a house with a basement that has a separate entrance, a detached garage that could be converted or a big lot where you could build a small cottage. This works great in areas with strong rental demand (think near universities, hospitals or downtown areas where young professionals want to live).

If you’re considering an ADUs or flex space, there are some important factors worth weighing before diving in. First up: Make sure there are enough bedrooms and bathrooms so everyone gets their own space (because nobody wants to navigate roommate bathroom schedules at 7:00 AM on a Monday). These renovations don't come cheap, though. Converting spaces or adding an ADU can eat up a significant chunk of budget so it's crucial to factor these expenses in from the start rather than treating them as afterthoughts. Then there's the bureaucratic fun: Zoning laws and mortgage financing rules. Converting single-family to multi-family isn't just adding a door and calling it good — local regulations and lender requirements can be surprisingly specific.

The smart move? Consult with a REALTOR® who knows the area, an appraiser, a contractor and a mortgage lender before making any commitments. This dream team helps navigate regulations and ensures your plans work within neighborhood rules and financial reality.

Common House Hacking Questions

1. Do I have to pay income taxes on my house hacking income?

Yes, rental income is taxable; however, it’s based on the net income. This means you can use deductions to lower the taxable amount generated by your rental property. Just remember that some expenses, like mortgage interest and real estate taxes, cover the whole property. You'll need to split these proportionally between your rental and personal use.

2. Is house hacking legal in all cities?

House hacking is legal but how you do it matters. "Rent-by-the-room" can sometimes hit "unrelated occupant" limits in certain areas. And here’s a big one: Always verify the legal unit count of a property you’re considering. That "three-bedroom with a basement apartment" might only be zoned as a single-family home, which means renting out that basement could technically be illegal.

Do your homework before you buy. Check zoning laws, talk to your REALTOR® and make sure you're playing by the rules. The last thing you want is to buy a property only to get hit with violations or fines.

3. Can I do this with a partner or spouse?

Absolutely. Many couples house hack duplexes to maintain private living spaces while still benefiting from the "half-off mortgage" effect. Some couples even house hack for a few years to build equity fast then move to a traditional home once they've built up enough wealth.

The Bottom Line

House hacking offers tremendous financial benefits but it's not the right strategy for everyone. Honestly evaluate whether house hacking aligns with your goals and situation.

House hacking may work exceptionally well for first-time homebuyers who prioritize wealth-building over lifestyle perfection, who are comfortable with delayed gratification and who view homeownership as an investment opportunity. If you're willing to sacrifice some privacy and convenience for some significant financial advantages, house hacking can accelerate your path to financial independence.

Just keep in mind that you’re taking on landlord responsibilities, managing tenant relationships and dealing with maintenance issues that affect your living situation directly. If you travel extensively for work or value absolute privacy, the stress might outweigh financial benefits.

Ready to Get Started?

1. Discuss the opportunity with a loan officer

Before you start scrolling through property listing, meet with a mortgage loan officer to discuss these questions and your homeownership goals. We'll help you understand exactly how much you can afford and guide you through every step of the mortgage process. The sooner you start the conversation, the sooner you can start building wealth instead of just paying rent.

2. Understand your financing options

You have more financing options than you might think. Your loan officer can help you identify the loans and programs you’re eligible for and walk you through the application processes.

3. Get pre-approved

Here’s the truth: In today’s housing market, you need a pre-approval letter. Getting pre-approved means a lender has reviewed your finances, credit history, income and debts and has committed to lending you a specific amount (subject to final underwriting, of course).

Connect with a mortgage loan officer today and we’ll help you navigate these three steps with confidence.