In October 2019, just before the Covid-19 pandemic hit the US, Nobel laureate Robert Shiller applied concepts from epidemiology (the study of epidemics) to economics in his latest book, Narrative Economics. Shiller argues that narratives, or stories matter to markets and to the broader economy. Here are a few of his key ideas:

- Narratives spread through a population the way a virus does.

- A powerful story can not only drive human behavior but influence economic events—and how we think about and remember those events.

- Economists can study narratives in their research to enhance the accuracy of economic forecasting.

Consider a simple example. If enough people believe the narrative that “hard times are coming,” then their own acts of preparing for hard times—such as slowing spending and increasing saving—could cause the hard times they so desperately fear and are trying to avoid. This observation runs counter to what most economists assume, all humans are rational economic actors who maximize utility and efficiency.

With that in mind, let’s look at three current narratives likely to drive discussions and behaviors in 2024.

The U.S. Presidential Election

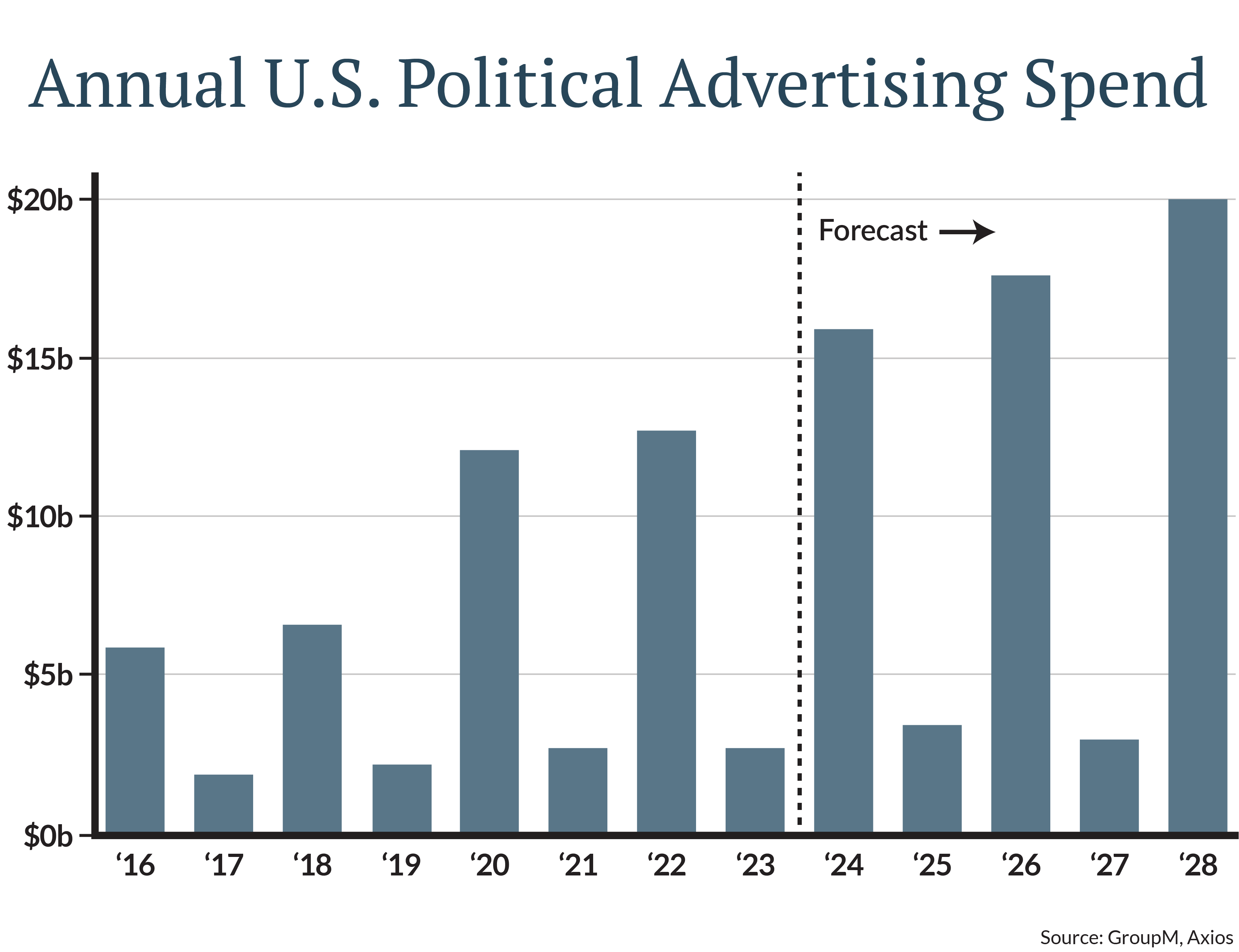

The 2024 election will dominate the news cycle this year. For good reason, spending on political advertising is expected to reach record levels—with some estimates of political ad revenue close to $16 billion. The news media will want its slice of that advertising pie.

The election will have important ramifications for the economy, but as my colleague Kyle Tripp wrote in Elections: Do they matter?, the impact of election outcomes on market performance are ambiguous at best. Investment winners and losers of an election are more likely to be determined at the individual company or industry level rather than the broader market.

Markets are not yet focused on the election narrative, but this will change. As we get closer to the election, it is possible equity market volatility will increase due to the uncertain outcome and uncertain policy changes. Markets despise uncertainty.

As an investor, the biggest risk from an election cycle is the sheer energy and emotion that it can bring out of people. Avoid making investment strategy changes when emotions are running high. Look for more election analysis in our “Decision 2024” video segment, premiering March 15 on the Johnson Financial Group website.

Artificial Intelligence

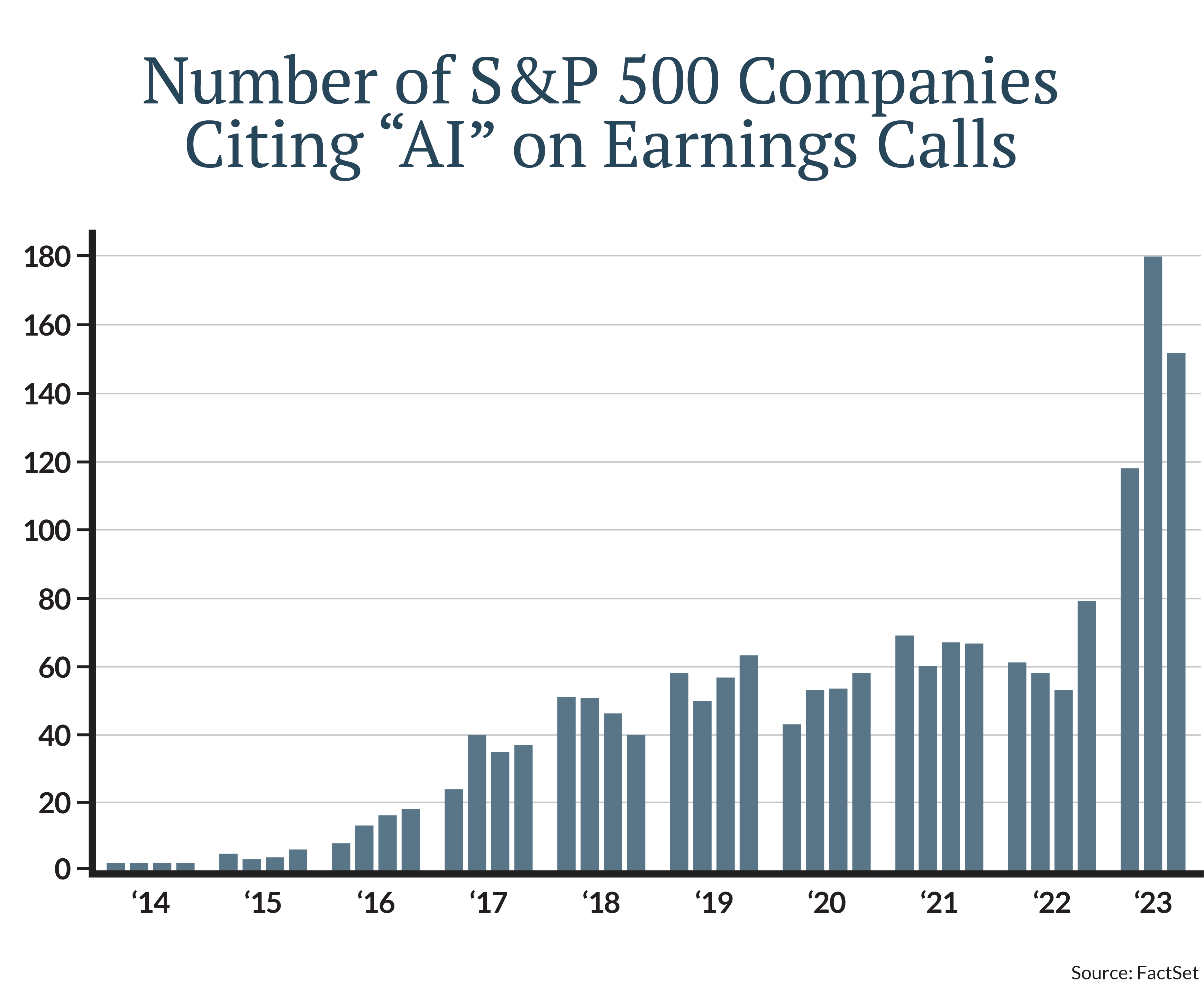

The AI narrative has been a significant boon to the economy and driving force in markets in 2024. JFG Director of Alternatives Jonathan Henshue discussed the topic last year, his piece Unraveling the Rise of AI.

This narrative has seemingly taken a dominant position in the financial markets. CEOs of public companies appear to be competing to see who can fit the most AI references into an earnings call (see accompanying chart). The AI boom has reminded some of the dot.com bubble in the late ‘90s, while other say “it’s different this time.” Like most things, the truth probably lies somewhere in the middle.

There is no doubt that companies are spending a lot of money building out AI infrastructure, but to what ends, and with what long-term impact, we have yet to find out. One thing is certain, AI will be part of the economic conversation for the foreseeable future.

The Taylor Swift Economy – “Swiftonomics”

I don’t understand the Taylor Swift obsession (and I probably never will) but my ignorance doesn’t make this narrative any less real. Some estimates peg Swift’s impact on the U.S. economy to be north of $5 billion. The Swiftonomics narrative epitomizes the trend of consumers shifting spending preferences from “stuff” to “experiences.”

TIME Magazine made the comparison that every weekend she is performing, it has the economic equivalent of two to three Super Bowls. Last summer, Swift even garnered a mention in the Federal Reserve’s “Beige Book” report of anecdotal economic conditions.

Of the three economic narratives we’ve reviewed here, Swiftonomics may be the best example of Robert Shiller’s thesis that economic impacts spread like epidemics. While the Jerome Powell-led Federal Reserve has garnered credit for engineering a soft landing (so far), perhaps Powell should share any accolades with Taylor Swift, whose global economic stimulus tour continues through the end of 2024.

What’s the Story?

These and other narratives will develop, intertwine, rev up, wind down and otherwise change as 2024 runs its course. New stories will emerge and take over. Some will spread like epidemics, and others won’t. What matters most for investors is keeping perspective—for example, that presidential politics don’t usually matter greatly at a broad level. So, as investors, we watch, and we seek to maintain our equilibrium.