Wealth Insights

Fed’s Warsh Era Begins with Hawkish Tone

6 minute read time

The Federal Reserve left interest rates unchanged at its June 17 meeting, but investors were more focused on the future under new Fed Chair Kevin Warsh, whom Trump appointed in May.

With President Trump blasting outgoing Fed Chair Powell unrelentingly for not cutting interest rates, many speculated that the next Fed Chair would need to promise rate cuts to get the job. But Kevin Warsh’s first meeting revealed that the committee he chairs is now leaning toward rate hikes rather than the multiple cuts expected just a few months ago. His hawkish tone was a surprise for some and markets began to solidify views that the Fed’s next move could be a 0.25 percentage point rate hike.

In their Summary of Economic Projections accompanying the decision, nine of nineteen Fed officials penciled in at least one rate increase by year’s end, up from none in March. Just one official foresaw a cut, down from twelve in March.

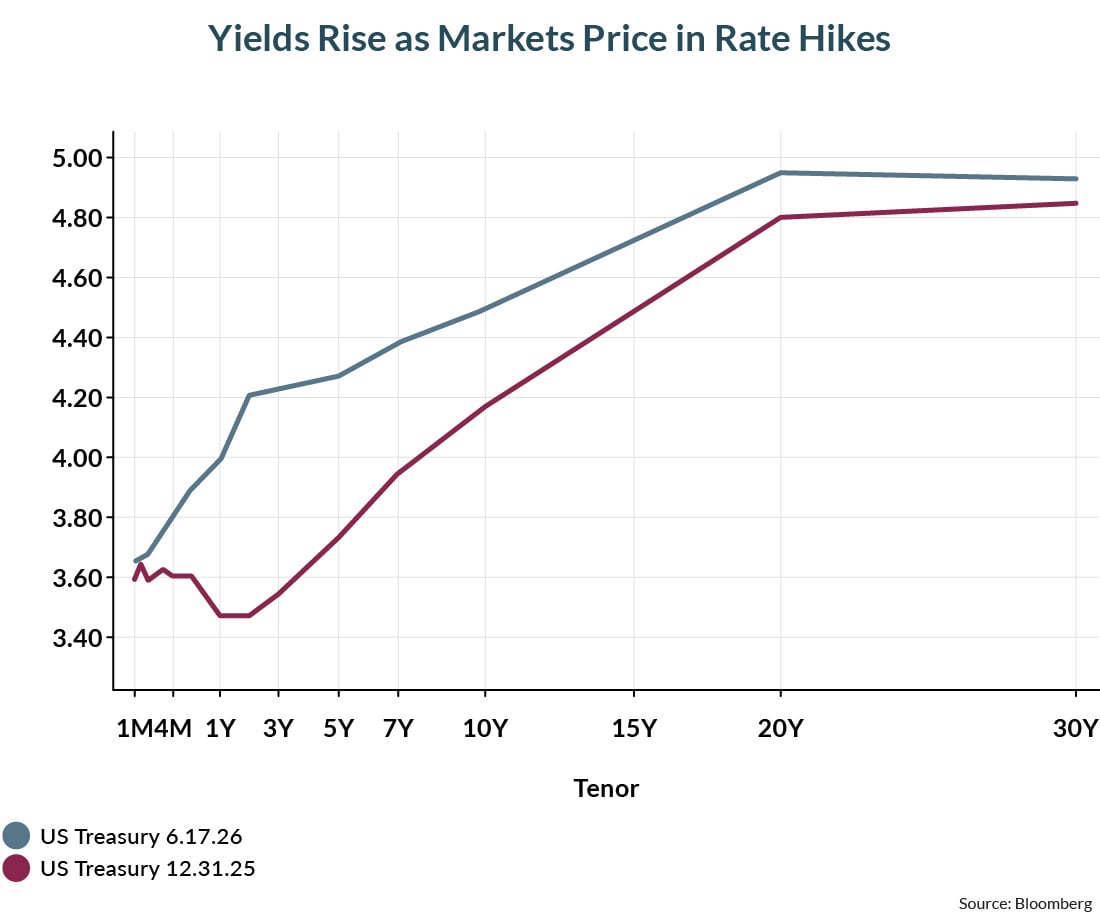

Bond markets had already begun to anticipate an oil-related resurgence in inflation that might force the Fed’s hand [Figure 1] and the selloff we have seen this year (bond prices decline when rates rise) continued after the decision. The two-year Treasury yield rose 0.11 percentage points to 4.16% in the aftermath of the decision, an indicator that markets expect the Fed to keep their focus on fighting inflation in the near term rather than supporting the labor market.

Yields Have Risen as Markets Price in Rate Hikes

While Warsh declined to provide his own projection of where rates might go, he did nothing to counter a hawkish interpretation of the decision. In fact, he reinforced it: “We recognize that inflation has been running well ahead of the Fed’s long-stated inflation goal of 2% that’s been going on for more than five years,” he said at his post-meeting press conference. “But the recent past need not be prologue. I am pleased to report that members of the FOMC [the Fed’s monetary policy committee] are unambiguous and unanimous: This committee will deliver price stability.”

A Different Kind of Change

If Warsh’s first meeting is a sign of things to come, it may mean that his tenure will be marked less by a dovish policy stance than by institutional changes. Warsh has long argued that the Fed should reduce the amount of “forward guidance” it provides markets, and in his first meeting as Fed chair, he implemented that vision.

The statement accompanying the Fed’s interest rate decision was cut dramatically, eliminating reference to the conditions the committee considers in its outlook for rates. Since 2008, Fed officials came to believe that by giving investors a heads-up on the central bank’s intentions for short-term interest rates, it could better steer longer-term rates and the economy. But by cutting the statement and declining to submit his own rate forecast, Warsh hinted at a Fed that that is likely to depart from the use of forward guidance as a policy tool.

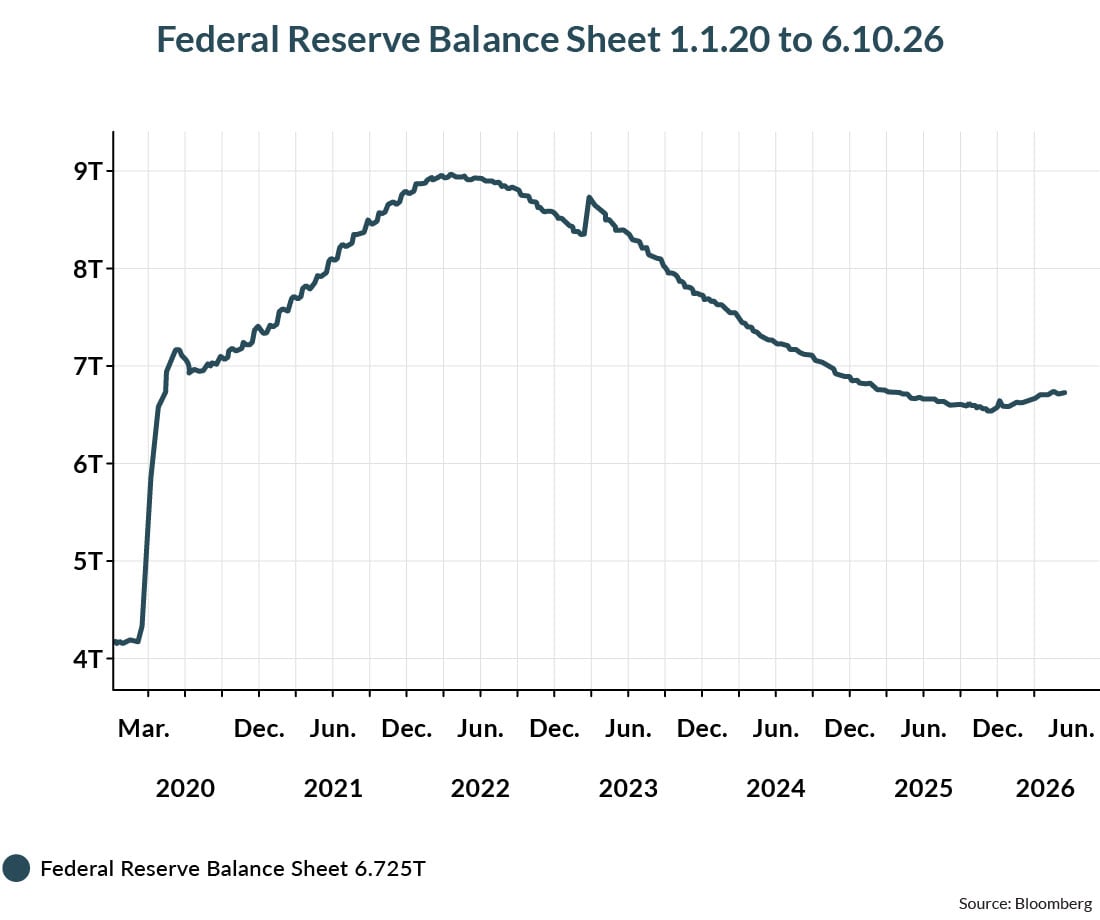

Warsh also announced that he is creating five task forces to examine everything from the way the Fed communicates to finding new, more timely data sources and looking at whether artificial intelligence is changing the productivity of the economy. The task force on the Fed’s balance sheet could prove consequential if Warsh’s desire to reduce the Fed’s asset holdings comes to fruition. The Fed’s balance sheet swelled in the wake of the 2008 financial crisis as it purchased Treasuries and mortgage-backed securities and it was used even more broadly to support asset prices during the pandemic [Figure 2].

Federal Reserve Balance Sheet Remains Bloated Post Covid

Warsh’s views on cutting the balance sheet are not mainstream among economists, and the combination of a smaller balance sheet and less communication could be seen by the market as signs of a diminished willingness of the Fed to intervene when markets decline. A reduced “Fed Put,” as this has become known, could have implications for investors and will be closely watched by market participants, including us.

Opportunity Amid Higher Rates

With interest rates rising this year and inflation ticking up, it is understandable why investors might be questioning their bond allocation. Two things are important to understand, however.

First, today’s higher yields function as a cushion to offset some of the price impact of the rise in interest rates and total returns for intermediate-term bonds are modestly positive this year despite rising yields and lower prices.

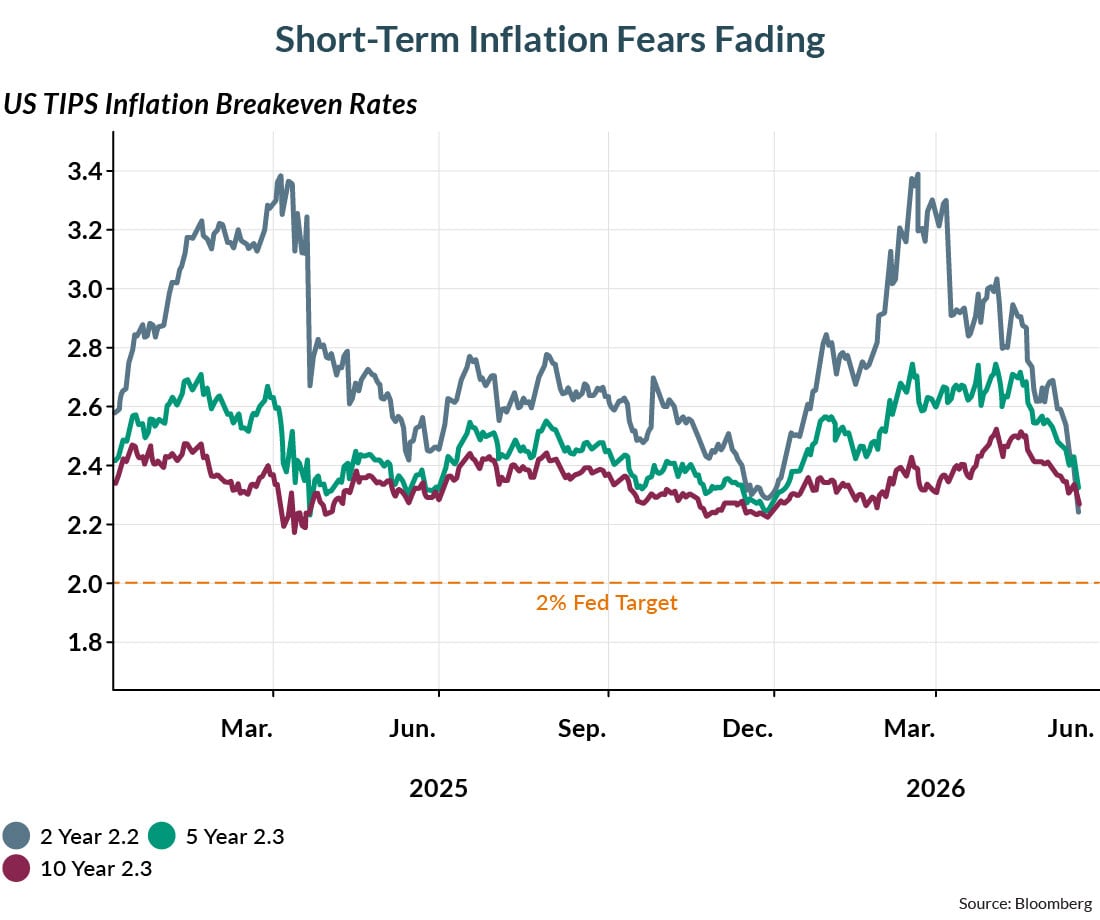

Second, longer-term inflation expectations appear to have peaked [Figure 3]. Treasury Inflation Protected Securities, or TIPS, now show investors think longer-term inflation will fall closer to the Fed’s 2% target as oil prices retreat and the Fed remains independent of politics. This means that investors buying bonds at 4%-5% today can capture returns well above expected inflation.

Inflation Expectations Appear to Have Peaked

Kevin Warsh’s hawkish tone at his first meeting as Fed Chair may have been a surprise to some, but investors should cheer a Fed that takes inflation seriously and maintains political independence. It will be a long time before we know what his legacy will be. In the meantime, we remain keen observers and look to capitalize on the opportunities markets give us as the new regime makes its mark.

This information is for educational and illustrative purposes only and should not be used or construed as financial advice, an offer to sell, a solicitation, an offer to buy or a recommendation for any security. Opinions expressed herein are as of the date of this report and do not necessarily represent the views of Johnson Financial Group and/or its affiliates. Johnson Financial Group and/or its affiliates may issue reports or have opinions that are inconsistent with this report. Johnson Financial Group and/or its affiliates do not warrant the accuracy or completeness of information contained herein. Such information is subject to change without notice and is not intended to influence your investment decisions. Johnson Financial Group and/or its affiliates do not provide legal or tax advice to clients. You should review your particular circumstances with your independent legal and tax advisors. Whether any planned tax result is realized by you depends on the specific facts of your own situation at the time your taxes are prepared. Past performance is no guarantee of future results. All performance data, while deemed obtained from reliable sources, are not guaranteed for accuracy. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Asset allocation and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment losses. Certain investments, like real estate, equity investments and fixed income securities, carry a certain degree of risk and may not be suitable for all investors. An investor could lose all or a substantial amount of his or her investment. Johnson Financial Group is the parent company of Johnson Bank and Johnson Wealth Inc. NOT FDIC INSURED * NO BANK GUARANTEE * MAY LOSE VALUE

ABOUT THE AUTHOR