Last week I had the opportunity to participate in a large gathering of Wealth clients at a luncheon in Racine. Many thanks to Kelly Mould for organizing the event. Here’s a snapshot of us in the beautiful event space—a former church—with co-presenter and Director of Wealth Strategy Joe Maier.

Joe packed his talk on the “Seven Deadly Sins of Investing” with carefully distilled wisdom (and more than one comment about distilled beverages). My presentation, by contrast, focused mostly on our market outlook for 2024.

After zeroing in on inflation (still stubborn), interest rates (probably higher for longer), the business cycle (which is really the profit-margin cycle … and profits need to rise to support stock prices), the Magnificent Seven and more, I turned to a trio of topics relating to risk.

Those three ideas—each with an accompanying image—are what I’d like to focus on in this week’s commentary.

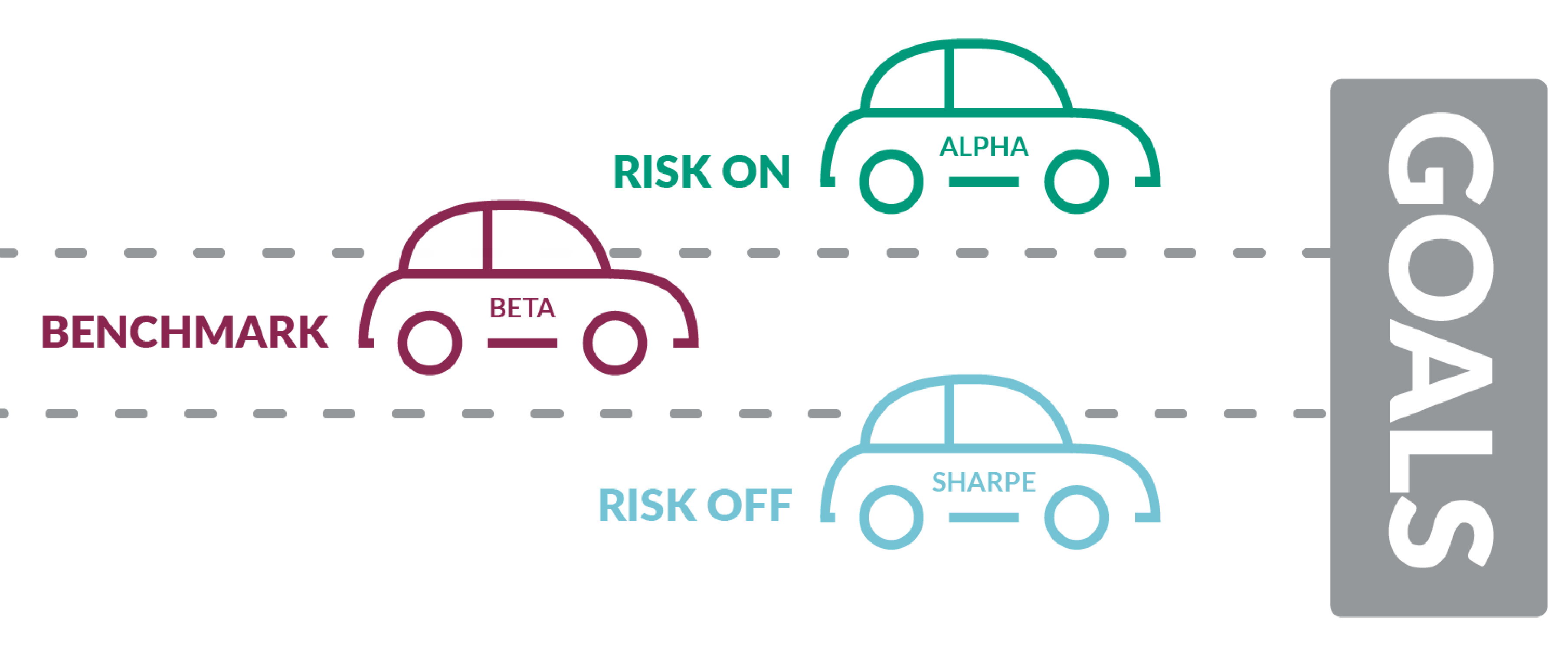

Risk as a three-lane road

Here’s a simple illustration. It’s a three-lane road. All three lanes are likely—based on historical data—to lead to the pre-established goal. That’s a critical point, so let me phrase it a different way for emphasis: An investor can reach the goal by driving in any of these three lanes.

Our job as an investment team is to properly define the center lane by selecting an investment benchmark appropriate for the investor. Then, over time, we consider shifting one lane over in either direction. But not two lanes! (It’s not shown in the illustration, but there are shark-infested waters on both sides of the road.)

Let’s break it down further to show why this is so important.

- The middle lane—or benchmark. Our capital market assumptions are built into your financial plan. As a result, your plan assumes a certain return and level of volatility. Your advisor can tell you the probability of success for your goals because we manage money to stay within the reasonable range of returns for your chosen portfolio.

The benchmark is a crucial piece of this process. The benchmark serves as our guidepost. The goal is not simply to beat the benchmark, the goal for us is to stay within a reasonable range of the benchmark. In fact, beating the benchmark by too much for any manager should raise a significant red flag. Trouncing the benchmark likely indicates that way too much risk was taken, or the benchmark itself is not an appropriate fit for the strategy.

- The “risk on” and “risk off” lanes. Based on our ongoing research we make adjustments to either increase or reduce risk in the portfolio. But we will only move one lane over on either side—because we know if we stay this course then all roads still lead to goal achievement.

By contrast, if we were to increase or decrease risk too much, then the car leaves the road (that’s where the shark-infested waters come in). The whole planning process breaks because the risk is no longer consistent with meeting the established goals.

Bottom line: Everything starts with goals. Then we identify the middle lane … and only then do we consider shifting to the left or right one lane as market conditions warrant.

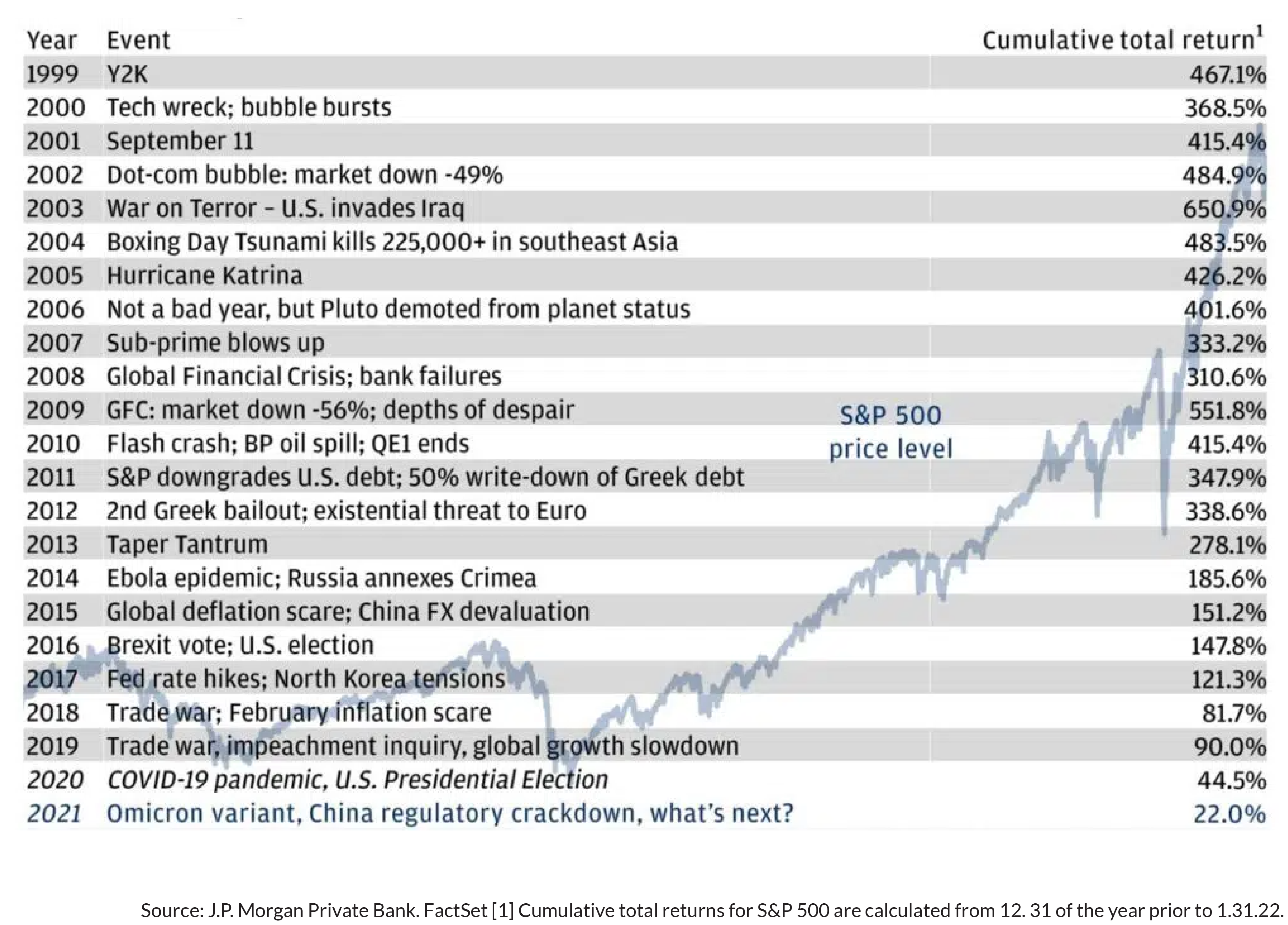

Every year has headline risk

There are always risks to investing—which are tempting to internalize as reasons not to invest. Investors use the phrase “headline risk” to refer to whatever news headlines are trumpeting as dangerous to your financial health.

Accepting headline risk allows patient investors to be rewarded with superior returns, as reflected by the following impact, which superimposes a chart of the S&P 500 Index of large-company stocks from 1999 through 2022 over a list of headline risks in each successive year during the period. The right-hand column shows an investors’ cumulative total return if they were to start investing in a particular year.

Looking down that right-hand column, you can see that—of course—certain years would have been better to start than others. But from any given headline risk, the impact to your psyche is likely bigger than the impact to your portfolio over the long term. The greater danger is staying away.

Bottom line: We avoid setting investment policy based on headline risk. If you’re riled by something happening in the markets and have a feeling you should do something, the thing to do is call your advisor. Your advisor can rerun the plan and ensure you’re still on the road to success.

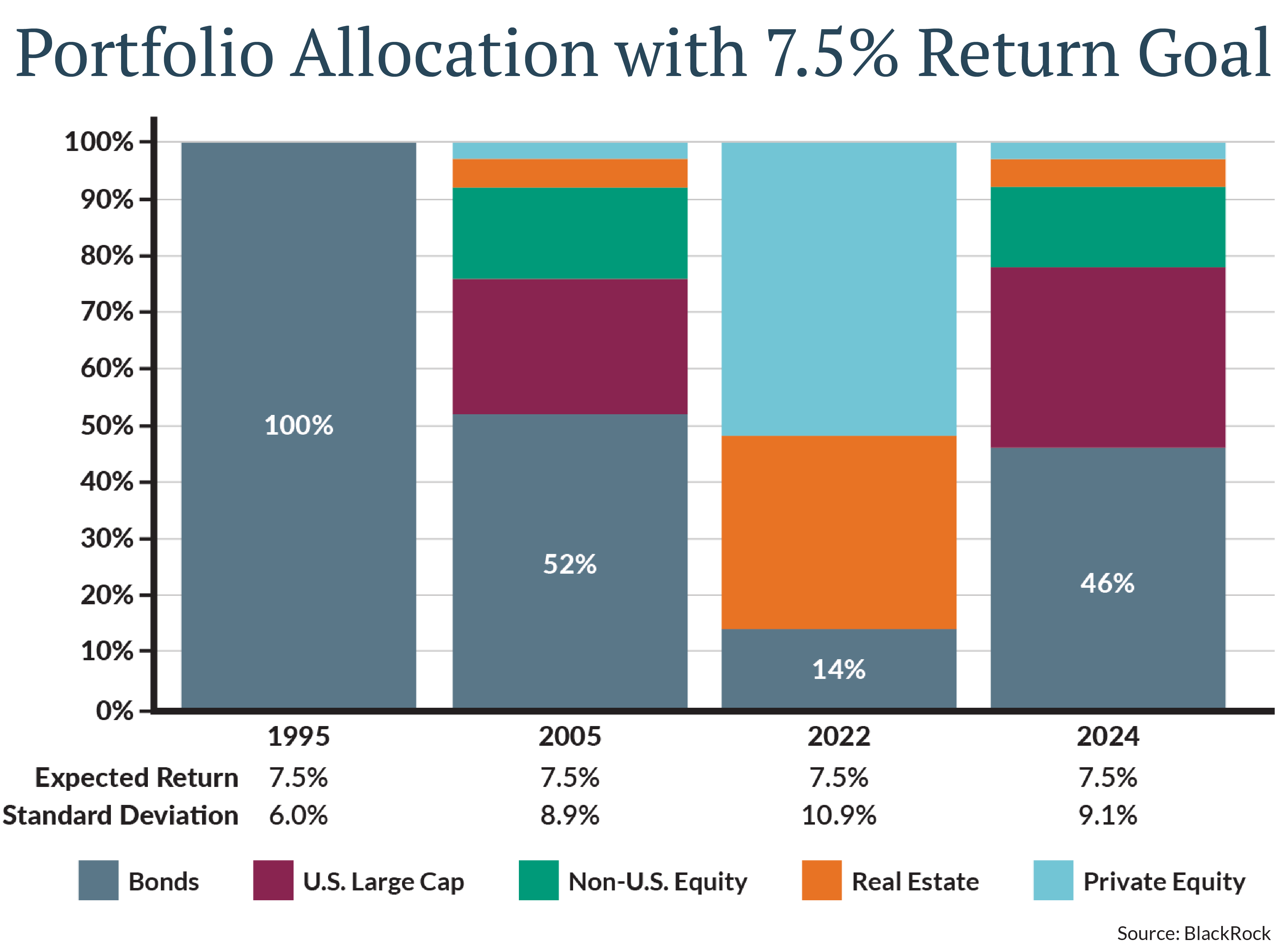

Risk and portfolio allocation

This is the most complex of the three images I’m sharing today, but the concept is simple. It points to the far more constructive role that bonds can play in a portfolio now versus just a year or two ago. Here’s what the chart conveys. Say your plan is built with a 7.5% return goal (average across asset classes) while minimizing volatility:

- In 1995, you could have invested 100% of your portfolio in bonds—so, relatively safe assets—and met your objective.

- 10 years later, in 2005, lower interest rates meant you could only allocate about half your portfolio to bonds.

- In 2022, you could have only dedicated 14% of your portfolio (as modeled in the chart) to the relative safety of bonds. In fact, to hit 7.5% that year, you would have needed to load up on real estate and private equity since stocks had a terrible year.

- Now, in 2024—with interest rates back to a far more normal range—you can once again allocate a substantial portion of a portfolio to the relative safety of bonds.

Bottom line: Bonds can once again be strong contributors both in generating investment returns and as portfolio diversifiers.

The change warrants a reassessment of risk allocations for investors, and we’re encouraging clients to evaluate their asset allocations in relation to their financial needs and return objectives. In short, many investors may be able to attain their financial goals with a more significant allocation to bonds.

Closing thought

Any discussion of risk is necessarily founded on understanding your individual goals. All the work we do as an investment team is about complementing the foundational work you do with your advisor, so I’d like to close with another shout-out to Joe Maier, Kelly Mould and the rest of our outstanding wealth advisory team.

Success requires far more than having investment knowledge. In my view, most of investment success is about identifying and sticking to optimal investment behaviors:

Speaking for the entire investment team, allow me to stress what a privilege it is to be part of your investment journey.